This was originally posted on Ventureburn on Feb. 14, 2017.

As an entrepreneur involved with two highly successful full-stack technology businesses, I spent fifteen years curiously wondering how venture capitalists make decisions. When I wasn’t focused on delivering value to customers and employees, I focused on how I could demonstrate that value to VCs in order to raise capital.

Often the process felt like it was shrouded in mystery—conjuring images of tribal gatherings, Shark Tank-like voting sessions and perhaps an Ouija board or two. Even after I secured capital with several of the best firms, I still felt like an element of luck was involved.

Now that I find myself on the other side of the table after founding my own VC firm, the mystery has been revealed. In short, I have discovered that successfully presenting your company is a skill that can be learned by understanding the venture capitalist point of view, and gaining clarity into the VC approach is different from understanding how to be an entrepreneur.

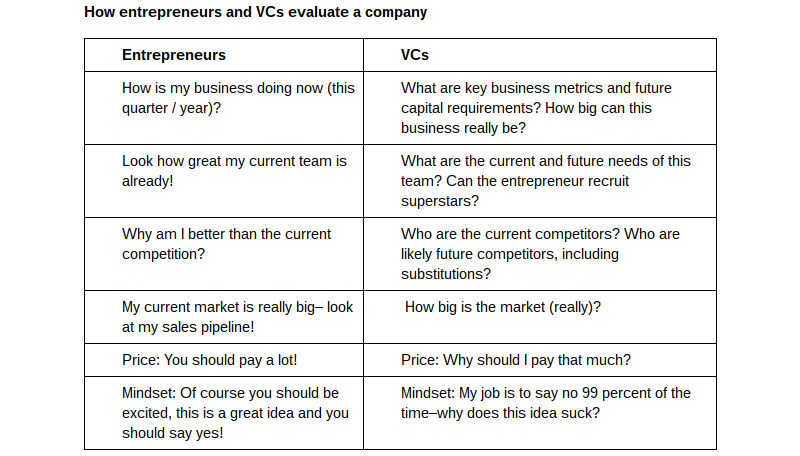

The biggest difference between an entrepreneur and a venture capitalist comes down to mindset. Entrepreneurs specifically tend to take an insider’s view of their business and then extrapolate that view to the market while venture capitalists do the opposite—take in the market landscape first. Understanding this difference is the key to securing critical capital necessary to keep dreams afloat.

The following chart illustrates what those views look like in practice:

The differences are subtle but important. Entrepreneurs that understand these framing devices can modify their approach to raising capital by crafting a compelling story that appeals to investors’ practical market sensibilities.

A winning story should address all of the following aspects:

1. Be conservative and detailed when you talk about the market you’re addressing.

1. Be conservative and detailed when you talk about the market you’re addressing.

Spend a significant amount of time thinking about who exactly will be your customers, making sure to differentiate between total available market, serviceable available market and serviceable obtainable market. Be accurate and realistic.

2. Give VCs a balanced view about potential competition.

Don’t just make a simple competitive landscape grid that magically depicts your business in the upper right quadrant. Instead, think deeply about current and future competitors, and show that your company has a plan to handle competitors as well as to discourage substitutes. Explain why you are winning today and why you will continue to win tomorrow.

3. Give VCs a view into the customer’s mindset.

Why are customers buying your product and how satisfied are they? What steps are you taking to maintain or increase that satisfaction? Explain to us what your average customer is thinking as they buy and use your product.

4. Help us understand how you are building your team.

We’ve already read your biographies and know about your past work experience but we are looking for more context. Be prepared to tell us why your current team is relevant to your strategy and talk openly about future executive needs.

5. Spend time on key business metrics, not just financials.

Financials are helpful, but at an early stage, money may not be the best indication of future success. Focus instead on spelling out the key unit economics that will be crucial to financial success as your business grows, such as gross margins, the cost of customer acquisition, and the lifetime value of a customer.

6. Be thoughtful about what could go wrong–both internally and externally.

My favourite question to ask is a simple one. Let’s say we are in a bar, two years from now, drowning our sorrows because this business failed … what happened? Think about external factors and internal factors. This isn’t being negative, it is being thoughtful and showing a critical mindset about how you will grow and expand your business and what obstacles you imagine you will have to overcome to do so.

7. Passion might not win the day, but it is incredibly important.

If you, as the entrepreneur, are not personally convinced that the idea you are pursuing is worth every waking moment of your professional life than you cannot expect others to get excited either. VCs are looking at both the idea and the entrepreneur’s personal commitment to making an idea a success. Do not underestimate how critical your passion, commitment and enthusiasm is to making your dream a reality.

An entrepreneur’s job is to educate potential investors

Any presentation that follows all of the above guidelines will help to close the massive information gap between an entrepreneur and a source of capital. Too often, entrepreneurs feel like venture capitalists “just don’t get it,” but this idea usually stems from the fact that no one has done a thorough job of explaining it to them. VCs’ tough questions or reticent attitudes are often just ways to push entrepreneurs to give a more comprehensive and outward-facing view.

An entrepreneur who gives potential investors what they want understands better how investors evaluate potential and assess risk. If you can show us that you understand and appreciate our interests and the VC point of view, we will be more eager to work with you to help you grow and improve your business in ways that appeal to the market.