How entrepreneurs and investors can use their respective insanity to work together and drive better alignment and results

(A version of this post appeared on Forbes)

Fund-raising is always tough. I originally wrote a version of this post a month ago to help entrepreneurs navigate the always trepid waters of fund-raising. In the past few weeks, with the outbreak of the COVID-19 pandemic, the challenges entrepreneurs face raising capital (along with everything else) have been magnified a hundredfold. Yes, you can still raise capital, but in these unprecedented times, it’s going to be a lot harder. Having been on both sides of the table in good times and bad, I’d thought I’d share some insights on how investors and entrepreneurs can work together in this uncertain environment. For some perspective, let me start by recounting two recent video conference calls…

At the end of a very long day, I logged out of my Zoom account for the day and shook my head. How did two video conference meetings on the same topic produce two totally different perspectives and agendas?

We were considering leading the Series A capital raise for a seriously innovative company. The first call, with a partner in another firm who was considering joining us in investing, was business-like, almost clinical. “This is a really exciting deal,” they said, “and we would be interested in investing if the valuation and terms make sense. Given this COVID-19 thing, we could probably jam them a bit more on terms, especially valuation.” Cold, impersonal and without emotion—just like any good serial killer in the Stephen King novels that fill my sleep with nightmares.

The second call, with the company’s founder, was packed with energy and emotion. “We want to build an amazing company, and we feel like we have established product-market fit,” they said. “With some more capital, we can continue to make our life mission a reality. Yes, COVID-19 is a real consideration but should have no long-term impact on our business model.” Highly emotional, passionate and enthusiastic—just like any of the great entrepreneurs who likewise must be partially insane to deal with maddening highs and lows of starting a business.

So, which was it? Was this a “deal” or a “life mission”? The answer depends on your perspective. Now, more than ever, it is incredibly important to understand the difference between the mindsets of the entrepreneur and the investor. As we all work through the panic, troubleshooting and adjusting financial projections, it is hyper-critical to be as balanced as possible. For both sides to achieve the outcome they’re looking for, it pays to understand the other side’s perspective. We all miss sports, among other things right now, so maybe a quick analogy will help…

The Golfer and the Quarterback

Sports fans know how to appreciate different perspectives. I like watching both golf and football (or at least I used to...now I try and remember what a live sporting event is actually like). But there’s a big difference in how Rory McIlroy (currently the #1 ranked professional golfer in the world) and Patrick Mahomes (Kansas City Chiefs quarterback and Super Bowl MVP) go about their jobs.

When McIlroy is about to tee off, he considers the variables (distance, wind, club selection, etc.) and then he takes an isolated action (the swing). When the ball leaves the club, the result is already determined, and he can only watch and contemplate the outcome. Even with a bad shot, he knows he’ll get 60-70 more shots that day. Consideration, decision and action, then watching the results and knowing that while each shot is important, no single shot will make or break the match. That’s the approach and mindset of an investor with a portfolio of investments to oversee.

Contrast that to a typical play in the NFL. Patrick Mahomes calls a play based on the current down and distance. He takes the snap, and all hell breaks loose. He must make multiple decisions based on the huge number of events quickly unfurling around him. After that play, he huddles with his team and quickly calls another one, all the while knowing one bad pass could cost him the game or he could be knocked unconscious—or worse—by a 350-pound linebacker who literally is trying to kill him. Chaos, uncertainty, making decisions on the fly: That’s a day in the life of a high-growth company. Every plan feels like it could be his last—he has no “portfolio”—and tomorrow seems like a meaningless consideration.

Rising Tensions at Investment Time

The contrasting approaches of investors and entrepreneurs meet head-on when it’s time for a company to raise a funding round. And if each side isn’t careful, what should be a momentous event in a company’s history can strain relations long after the deal is done.

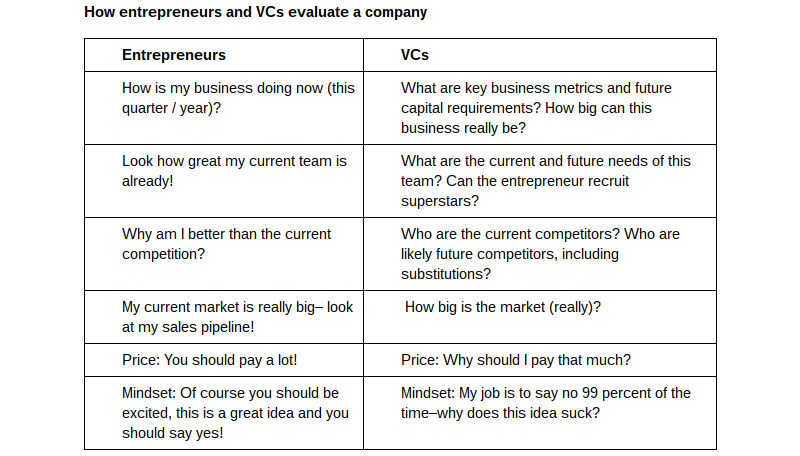

It begins with the process of determining a point estimate, essentially the best guess at how much the company is worth. It’s almost ridiculously difficult, building a specific business case that takes into consideration terms, price, ownership and dozens of other factors. When markets and valuations are experiencing incredible volatility - as they are now - these differences get magnified dramatically. But the process is critically important to the investors. The sad part is that 99% of an investor’s success will be determined by the investment she chooses to make and the price that is to be paid for that investment. Just about everything else is noise.

While entrepreneurs are certainly on board for any deal that maximizes their price and minimizes the dilution of their shares, they also know that the details really won’t matter that much if they execute on their vision and plan. They don’t see much point in painstakingly determining a fixed point estimate when conditions change every day. The bulk of her success will be determined by the execution during the years after the investment—and if she is successful, the valuation and price paid at the time of the investment will be largely meaningless.

See the contrast inherent here?

It’s also critically important to note that investors are dealing with a portfolio of companies. They can afford to be wrong every now and then, provided there’s a big win mixed in along the way. For entrepreneurs, the success of their business is all or nothing. There’s nothing for them to fall back on. This simple fact can magnify an already conflict-ridden environment.

A Simple Solution For Both

When we consider leading an investment, we try to do a couple of simple things to bridge the gaps between us (as investors) and the entrepreneurs we are backing. It starts with an open dialogue. We sit down with the entrepreneur before any investment and share our business plan, our perceived investment risk and our expected valuation outcome for their company.

We also ask the entrepreneur to share with us what he or she most wants to happen with the business over time: hopes, dreams, aspirations and best-case and worst-case outcomes. At the end of this discussion, my favorite thing to do is to ask the entrepreneur one simple question. “Five years from now, we are sitting in a bar, and we are either celebrating a great success or drowning our sorrows. Tell me why either happened.” This question more than any other helps both of us get a shared view on what could go right AND what could go wrong – and start the relationship from the same perspective on both.

“Five years from now, we are sitting in a bar (not watching each other sip beer on our webcams), and we are either celebrating a great success or drowning our sorrows. Tell me why either happened.”

We also ask the entrepreneur to share with us what he or she most wants to happen with the business over time: hopes, dreams, aspirations and best-case and worst-case outcomes. At the end of this discussion, my favorite thing to do is to ask the entrepreneur one simple question. “Five years from now, we are sitting in a bar, and we are either celebrating a great success or drowning our sorrows. Tell me why either happened.” This question more than any other helps both of us get a shared view on what could go right AND what could go wrong – and start the relationship from the same perspective on both.

We also write an investment memo for every deal and share it with the entrepreneur. The memo spells out our thoughts on the deal—both the upsides and downsides—so that there’s full transparency.

When we do this, we get reactions like, “Holy cow. Thank you! I never understood how this works, and this helps me plan my business and board updates accordingly.” The entrepreneur understands our perspective, risks we see in the business and the outcome we are focused on achieving. From day one, we have a shared perspective.

Both a Hole-In-One and a Touchdown Are Worth Celebrating

The very best investor-entrepreneur relationships are based on trust and openness, along with a shared vision, goals and expectations.

It’s so important for entrepreneurs to know the key assumptions, financial metrics, and risk factors that the investors are considering. It might be scary to hear, but it establishes the right level of trust and communication with the investment team.

It is equally important for investors to get into the mind of the entrepreneur and understand what she does (and does not) want to do with the business over time.

A shared perspective and understanding not only builds trust and openness from day one, but it also provides a shared viewpoint when things do and do not go as planned. Maybe, just maybe, it can also cut down on the therapy bills for both—but that concept will require a much, much longer blog post to really do it justice!

In fact, AlertMedia recently helped dozens of their customers communicate during Hurricane Harvey, mitigating loss and improving safety outcomes for people during this natural disaster.

In fact, AlertMedia recently helped dozens of their customers communicate during Hurricane Harvey, mitigating loss and improving safety outcomes for people during this natural disaster.

We also believe that Austin is THE best place for an entrepreneur to start and build a business, or as we like to call it: The Next Coast of innovation. This is where SXSW comes in. We think that it embodies the spirit, ethos and crucial content that drives this entrepreneurial activity.

We also believe that Austin is THE best place for an entrepreneur to start and build a business, or as we like to call it: The Next Coast of innovation. This is where SXSW comes in. We think that it embodies the spirit, ethos and crucial content that drives this entrepreneurial activity.

1. Be conservative and detailed when you talk about the market you’re addressing.

1. Be conservative and detailed when you talk about the market you’re addressing.

To be a great entrepreneur and leader, it takes courage, confidence and a willingness to do what others have not been able to do in the past. This is all good stuff.

To be a great entrepreneur and leader, it takes courage, confidence and a willingness to do what others have not been able to do in the past. This is all good stuff.